Brazil has emerged as the primary hub for digital infrastructure in Latin America, driven by a massive surge in cloud adoption and artificial intelligence requirements. For multinational corporations and hyperscalers, understanding Accounting for Data Centers in Brazil is the critical first step toward a successful market entry. The complexity of the Brazilian tax system, combined with the 2026 transition toward a new Value Added Tax framework, necessitates a sophisticated approach to financial management. This article explores the essential accounting and tax considerations for those evaluating Brazil as a strategic location for data center operations.

Strategic Structuring of the Legal Entity in Brazil

Choosing the correct corporate structure is the foundation of digital infrastructure projects. Most foreign investors opt for either a Sociedade Limitada (Limited Liability Company) or a Sociedade Anônima (Corporation). While the Limitada is often simpler to manage, the Sociedade Anônima is frequently preferred by digital infrastructure funds and hyperscalers due to its flexibility in issuing debt instruments and attracting diverse capital sources.

From an accounting perspective, the choice of tax regime is even more consequential. Multinational groups operating data centers almost exclusively utilize the Lucro Real (Actual Profit) regime. This regime is mandatory for companies with annual revenues exceeding R$ 78 million and is highly beneficial for capital intensive businesses. Under Lucro Real, the Corporate tax Brazil data center obligations are calculated based on net accounting profit, allowing for the full deduction of operational expenses and the utilization of tax losses from previous periods to offset future liabilities.

Corporate Tax Structure and Revenue Taxation

The Brazilian corporate tax landscape is characterized by its high granularity. For a data center operator, the primary direct taxes include:

- IRPJ (Corporate Income Tax): A base rate of 15% plus a 10% surtax on annual profits exceeding R$ 240,000.

- CSLL (Social Contribution on Net Profit): A standard rate of 9% for the technology sector.

The Impact of Tax Reform on Revenue

As of early 2026, Brazil is in the midst of a historic shift toward a dual Value Added Tax system. This transition significantly affects Brazil data center tax compliance. The legacy system, which relied on PIS and COFINS (federal social contributions) and ISS (municipal service tax), is being replaced by:

- CBS (Contribution on Goods and Services): A federal VAT that consolidates PIS and COFINS.

- IBS (Tax on Goods and Services): A sub national VAT that replaces the municipal ISS and the state ICMS.

For cloud infrastructure accounting Brazil, the transition means that the previous 9.25% cumulative rate of PIS and COFINS is shifting toward the new CBS rates. The IBS will gradually replace the municipal ISS, which typically ranges from 2% to 5% depending on the city. The most critical advantage of this new system for data centers is the full non cumulative credit mechanism. This allows operators to recover taxes paid on all inputs, including electricity and hardware, more effectively than under the previous fragmented system.

Tax Incentives and the REDATA Regime

To further solidify its position as a digital leader, the Brazilian government recently approved the REDATA (Special Tax Regime for Data Center Services). This initiative provides significant relief for digital infrastructure Brazil by addressing the high cost of hardware.

REDATA Benefits and Obligations

Under REDATA, qualified companies enjoy a suspension of federal taxes on the domestic purchase and importation of equipment, electronic components, and infrastructure materials. This includes the suspension of the Import Tax (II), IPI (Tax on Industrialized Products), and the federal contributions (PIS and COFINS) during the project phase.

To qualify for REDATA, investors must meet specific requirements:

- Sustainability: Data centers must utilize renewable or clean energy sources and meet strict water efficiency standards.

- Local Market Commitment: At least 10% of the processing and storage capacity must be made available to the domestic market.

- R&D Investment: Companies must invest at least 2% of the value of the incentivized products in local research, development, and innovation projects.

This regime is a game changer for the cloud infrastructure accounting Brazil landscape, as it significantly reduces the initial cash outflow required for facility construction.

CAPEX vs OPEX Data Center Strategy in Brazil

The decision between a capital expenditure (CAPEX) heavy model versus an operational expenditure (OPEX) model is a central pillar of Accounting for Data Centers in Brazil.

The CAPEX Approach

Hyperscalers and large cloud providers often prefer to own the physical infrastructure. In the Brazilian context, this involves massive investments in imported servers, cooling systems, and power substations. Under IFRS compliance Brazil (specifically CPC 27/IAS 16), these assets are recorded on the balance sheet and depreciated over their useful lives. Typical depreciation rates for IT equipment in Brazil range from 20% per year, while buildings are depreciated at 4% per year.

The benefit of the CAPEX model under the Lucro Real regime is the ability to use these depreciation expenses to reduce the taxable profit for IRPJ and CSLL purposes. Furthermore, the newly implemented tax reform allows for faster recovery of VAT credits on capital goods, improving the internal rate of return for these projects.

The OPEX Approach

Colocation and managed services providers offer an OPEX alternative. For a tenant, the monthly service fee is fully deductible as an operational expense. This approach is attractive for technology companies that want to scale rapidly without the burden of managing physical assets or dealing with complex import procedures.

From an accounting standpoint, the adoption of IFRS 16 (CPC 06 R2 in Brazil) means that long term lease contracts for data center space must be recognized as right of use assets on the balance sheet, with a corresponding lease liability. This blurs the traditional line between CAPEX and OPEX, requiring a sophisticated analysis of how these contracts affect financial ratios and covenant compliance.

Energy Cost Accounting and Sustainability

Electricity is the single largest operational cost for any data center. In Brazil, Energy cost accounting data center strategies are influenced by the liberalization of the energy market. As of 2026, many operators have migrated to the Free Energy Market (Mercado Livre de Energia), allowing them to negotiate prices directly with generators and focus on renewable sources.

Tax Credits on Energy

A common challenge in Data center accounting services is the treatment of ICMS (State Value Added Tax) on energy. Historically, only “industrial” companies could recover ICMS credits on electricity used in the production process. Data centers, being classified as service providers, often faced hurdles in claiming these credits. However, recent jurisprudence and the transition to the IBS (sub national VAT) are creating a more favorable environment where energy is increasingly viewed as an essential input, allowing for broader credit recovery and reducing the effective energy cost by up to 25%.

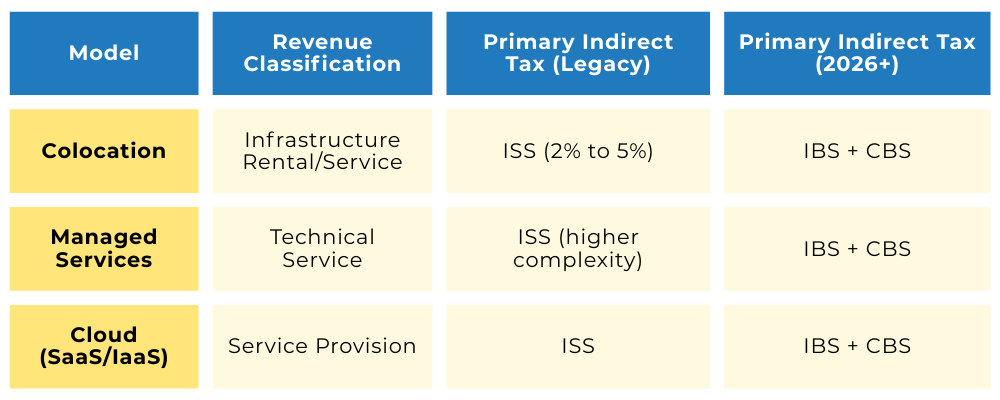

Colocation vs Managed Services vs Cloud Accounting

The accounting treatment in Brazil varies significantly depending on the business model. This distinction is vital for Colocation accounting Brazil and cloud operations.

In the legacy system, the distinction between a “rental” (not taxed by ISS) and a “service” (taxed by ISS) was a frequent source of litigation. The new VAT system aims to eliminate this ambiguity by taxing both goods and services under a unified rate, providing more legal certainty for operators.

Transfer Pricing and International Compliance

For multinational groups, Transfer pricing considerations are paramount. Brazil recently aligned its transfer pricing rules with the OECD guidelines through Law 14,596/2023. This shift requires data center operators to ensure that intercompany charges for management fees, technical support, and intellectual property licensing are conducted at arm’s length.

Accounting teams must prepare extensive documentation, including the Master File and the Local File, to justify the pricing of services shared between the global headquarters and the Brazilian subsidiary. Failure to comply can lead to significant adjustments in the taxable base and heavy penalties.

Compliance Risks and Audit Exposure

Operating in the Brazilian digital infrastructure sector carries unique compliance risks. The Brazilian Federal Revenue Service (Receita Federal) utilizes a sophisticated digital oversight system known as SPED (Public Digital Accounting System). Every invoice, accounting entry, and tax calculation is transmitted to the government in real time.

Key Risks for Data Centers

- Import Valuation: Auditors closely scrutinize the declared value of high tech equipment to ensure there is no under invoicing to avoid import duties.

- Split Payment Mechanism: The 2026 tax reform introduces a “split payment” system where the VAT (CBS/IBS) is automatically withheld at the moment of the financial transaction. This requires seamless integration between accounting software and banking platforms.

- Incentive Compliance: Under REDATA, failing to meet R&D or sustainability targets can lead to the retroactive cancellation of tax benefits, resulting in massive liabilities plus interest and fines.

Engaging specialized Data center accounting services is essential to navigate these digital audits and ensure that all ancillary obligations are met without error.

Strategic Conclusion

Brazil offers an unparalleled opportunity for digital infrastructure expansion, supported by a vast renewable energy matrix and a government committed to attracting high tech investment through the REDATA regime. However, the complexity of the ongoing tax reform and the rigorous digital compliance environment mean that a generic approach to accounting will not suffice.

The successful deployment of a data center in Brazil requires a deep understanding of the interplay between CAPEX strategies, VAT credit recovery, and OECD aligned transfer pricing. Investors must treat Accounting for Data Centers in Brazil not merely as a back office function, but as a strategic asset that can significantly enhance profitability and reduce operational risk. Partnering with specialized advisors who understand the nuances of the digital infrastructure sector is the only way to ensure long term success in this vibrant market.

Would you like me to draft a more detailed breakdown of the specific REDATA sustainability reporting requirements or create a comparative table of electricity costs across different Brazilian states?

0 Comments