🎧 Prefer to listen?

We break down CFEM, mining taxes and accounting challenges in Brazil in this quick podcast episode.

Introduction

Brazil is a major global mining jurisdiction. U.S. Geological Survey data lists Brazil among leading producers of iron ore, bauxite and gold—minerals that feed steel, aluminum and bullion markets.

This scale (and the investment pipeline described by the Brazilian Mining Institute (IBRAM) attracts foreign investors, but the compliance environment is complex: mining titles, environmental licensing, and multiple layers of taxes plus a mining royalty.

So, “accounting for mining companies in Brazil” is not just bookkeeping. It is the operating system that connects your mine plan to permits, cash flow, audits and investor reporting.

How mining operations work in Brazil

A simplified life cycle is:

Exploration → research authorization → mining concession → extraction → processing/beneficiation → commercialization.

Two legal milestones drive most accounting and tax decisions:

Research authorization (Autorização de Pesquisa / Alvará). ANM describes it as the regime for geological and technical work to define and evaluate the deposit and assess feasibility, granted through an administrative authorization.

Mining concession (Concessão de Lavra / Portaria de Lavra). After the final research report is approved, the Portaria de Lavra is the title that authorizes extraction, beneficiation and commercialization.

Two common foreign-investor doubts:

Do we need a Brazilian company to hold the mining rights? Usually yes. The Mining Code provides that research authorizations and mining concessions are granted to Brazilians or to a company organized in Brazil as a mining enterprise.

When does environmental licensing become “mandatory”? Early. The government’s mining concession guidance states that granting the Portaria de Lavra depends on presenting the competent environmental license.

Brazil mining regulation and the ANM

The federal mining regulator is the Agência Nacional de Mineração (ANM), which regulates, grants and supervises mineral activities (including mineral research and mining).

Foreign entrants usually confront three connected rule sets:

Mining Code framework. Decree‑Law 227/1967 defines the title regimes, including authorization and concession.

ANM procedures. ANM issues operational rules (systems, filings, administrative procedures) and supervises CFEM collection.

Environmental licensing. The licensing framework includes CONAMA Resolution 237/1997 and Complementary Law 140/2011, with licensing handled by one competent government level (federal, state or municipal).

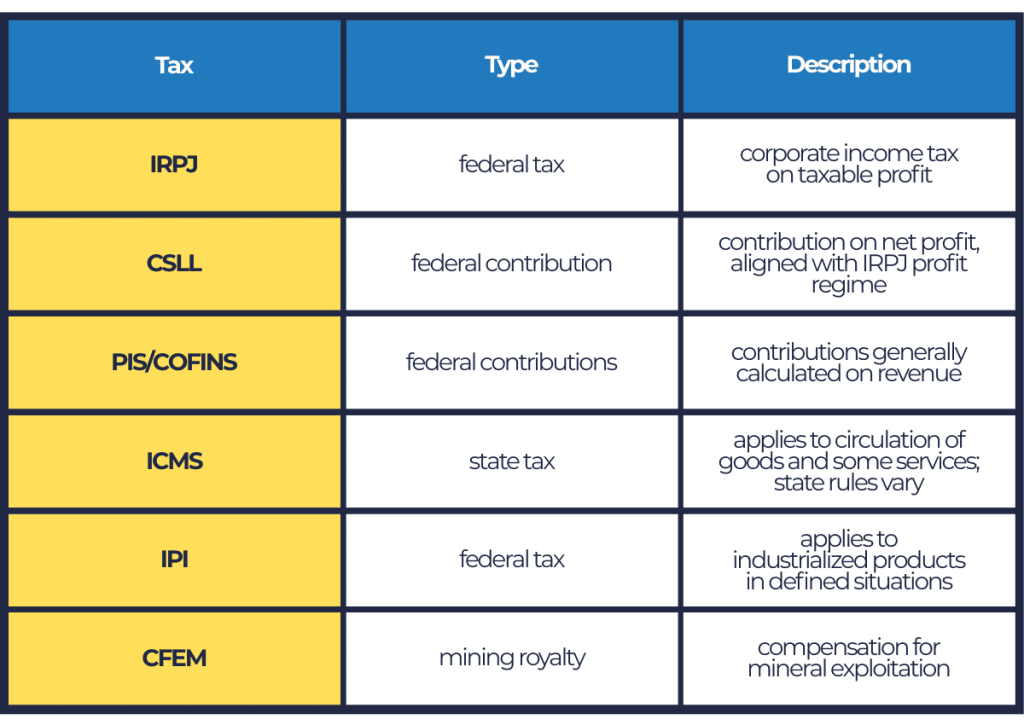

Main taxes paid by mining companies in Brazil

Brazil mining taxation has two layers: general corporate taxation and sector-specific royalties. When mapping taxes for mining companies Brazil, start here:

Practical explanations in plain English:

IRPJ (corporate income tax). Receita Federal do Brasil explains IRPJ is calculated based on profit regimes (real, presumed or arbitrated), with a standard 15% rate plus an additional 10% above a monthly threshold.

CSLL (profit contribution). CSLL is also profit-based; the Federal Revenue Service notes a 9% rate for most companies and that CSLL calculation follows the same regime adopted for IRPJ.

PIS/COFINS (revenue contributions). Legally, these contributions are calculated on company revenue (“faturamento/receita bruta”), and companies record them digitally through EFD‑Contribuições (covering both cumulative and non‑cumulative regimes).

ICMS (state tax on circulation). ICMS applies broadly to goods circulation and certain services; exports have constitutional non-incidence, so export operations often focus on credit management and documentation.

IPI (industrialized products). Federal rules define IPI bases both for internal operations and imports.

CFEM (mining royalty). CFEM is not an income tax; it is a mining-specific payment with its own base, rates and monthly deadlines.

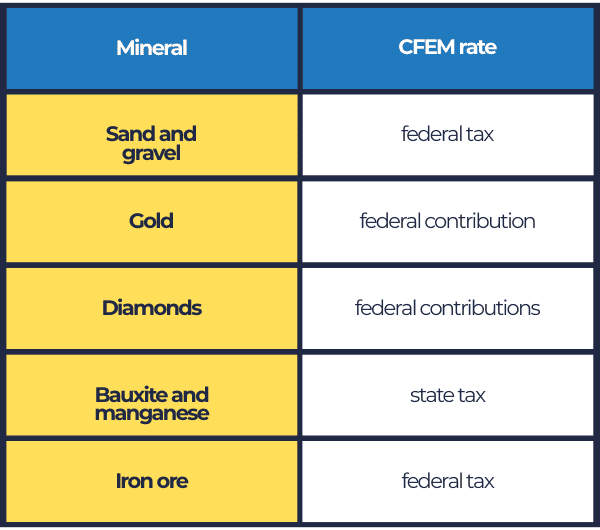

CFEM mining royalty Brazil

CFEM means Financial Compensation for the Exploitation of Mineral Resources. ANM explains CFEM is triggered in events such as first sale, certain first acquisitions, auctions, and mineral consumption.

How it is calculated (simple view). For sales, CFEM generally applies on gross sale revenue minus taxes on commercialization; export rules can use a minimum “parameter price” defined by the Federal Revenue Service when applicable.

Payment deadline. CFEM is paid monthly, due by the last business day of the second month after the triggering event.

Reference rates (selected minerals).

Distribution (high level). ANM summarizes that CFEM is distributed mainly to producing municipalities (60%), producing states (15%) and affected municipalities (15%), with the remainder allocated to federal bodies and sector funds.

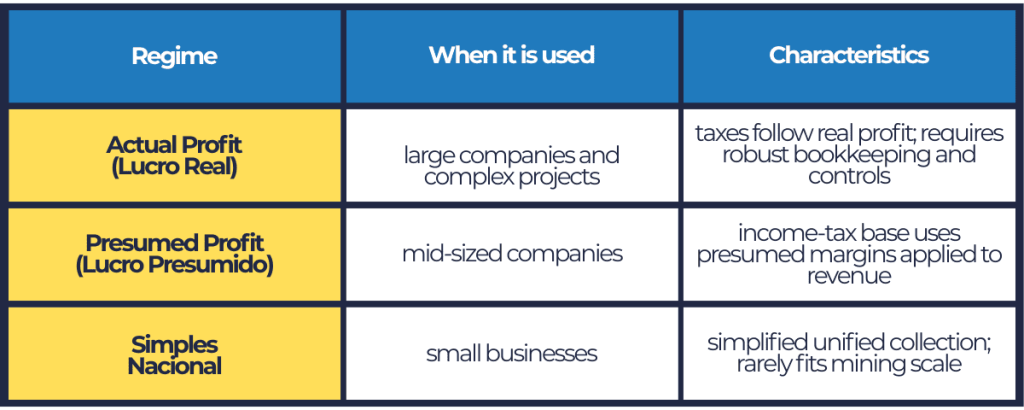

Accounting regimes, key challenges and the tax reform

Profit regimes. Foreign investors usually compare:

The Federal Revenue Service notes IRPJ is calculated based on profit regimes such as real and presumed profit.

Key accounting challenges in mining accounting Brazil tend to be control-heavy:

- Reserves and impairment: IFRS 6 sets requirements for accounting and impairment assessment around exploration and evaluation assets; Brazil applies IFRS through a local endorsement/enforcement structure.

- CFEM accuracy: requires reconciliation between invoicing, deductible taxes in the base, export pricing rules, and monthly payments.

- Asset lives and unit costs: heavy equipment depreciation, stripping/waste removal, and spend allocation across mine–plant–logistics materially affect unit economics; IFRIC 20 addresses production-phase stripping costs in surface mines.

Tax reform impact. Complementary Law 214/2025 instituted IBS, CBS and the Selective Tax, and Complementary Law 227/2026 sets governance/administrative rules for IBS. The Ministério da Fazenda describes the core shift: legacy consumption taxes (including PIS, Cofins, IPI, ICMS and ISS) are replaced by CBS (federal) and IBS (state/municipal), with a transition that includes a test year (2026) and phased rollout.

The Constitution also allows a Selective Tax on production/extraction of goods and services considered harmful to health or the environment; for extraction it is charged regardless of destination with a maximum rate of 1% of market value, and it does not apply to exports.

Expert insight. Marcos Ribeiro, director at CLM Controller, highlights that reform transitions require operational adaptation:

“ERP updates, new tax routines, team training, and contract reviews [are] necessary to avoid errors.”

He also stresses early planning:

“Adjusting processes in advance reduces non‑compliance risks and can uncover legal opportunities to reduce the tax burden.”

Best accounting practices for mining companies. Foreign operators tend to do best when they implement a CFEM “engine” integrated with invoicing and exports, disciplined cost accounting by mine phase, IFRS-aligned accounting policies, and tax reform readiness (systems, training, contract clauses).

Conclusion. Treating accounting and tax as part of mine governance (not a back office) helps reduce tax risk, avoid avoidable delays, and improve decision-making from exploration to production.

Institutional section. CLM Controller is a consulting and accounting firm based in São Paulo that supports international companies operating in Brazil with accounting outsourcing, tax advisory, financial consulting, regulatory compliance, and international business support (including reporting adapted to headquarters needs).

FAQ

What taxes do mining companies pay in Brazil?

Typically IRPJ, CSLL, PIS/COFINS, ICMS (depending on operations), IPI in relevant cases, plus CFEM as the mining royalty.

What is CFEM in mining?

A monthly royalty-like payment tied to mineral exploitation (e.g., first sale), with mineral-specific rates and a calculation base summarized by ANM.

How does Brazil tax mineral exports?

Exports generally have ICMS non-incidence, while CFEM has specific export base rules; strong documentation is essential.

Which accounting regime is best for mining companies?

Large mining projects commonly use Lucro Real because it follows real profit and supports stronger accounting controls and investor reporting.

Do foreign mining companies need a Brazilian company?

Generally yes, because mining titles are granted to Brazilians or companies organized in Brazil as mining enterprises.

0 Comments