Introduction

Importing goods into Brazil has long been known for its complex and high-cost structure. Starting in 2026, Brazil’s import costs are changing due to a convergence of new tax laws and operational reforms. Brazil passed a sweeping tax reform (Constitutional Amendment 132/2023) to simplify its notoriously complex tax system, replacing five different taxes with a new dual VAT model over the coming years. Additionally, authorities are rolling out new digital customs systems and adjusting regulations, all while global logistics volatility and currency fluctuations continue to influence the landed cost of imports. Foreign investors, importers, and international traders need to prepare now – understanding the new costs of importing into Brazil in 2026 is key for effective pricing and supply chain planning.

Overview of the Brazilian Import Cost Structure (2026)

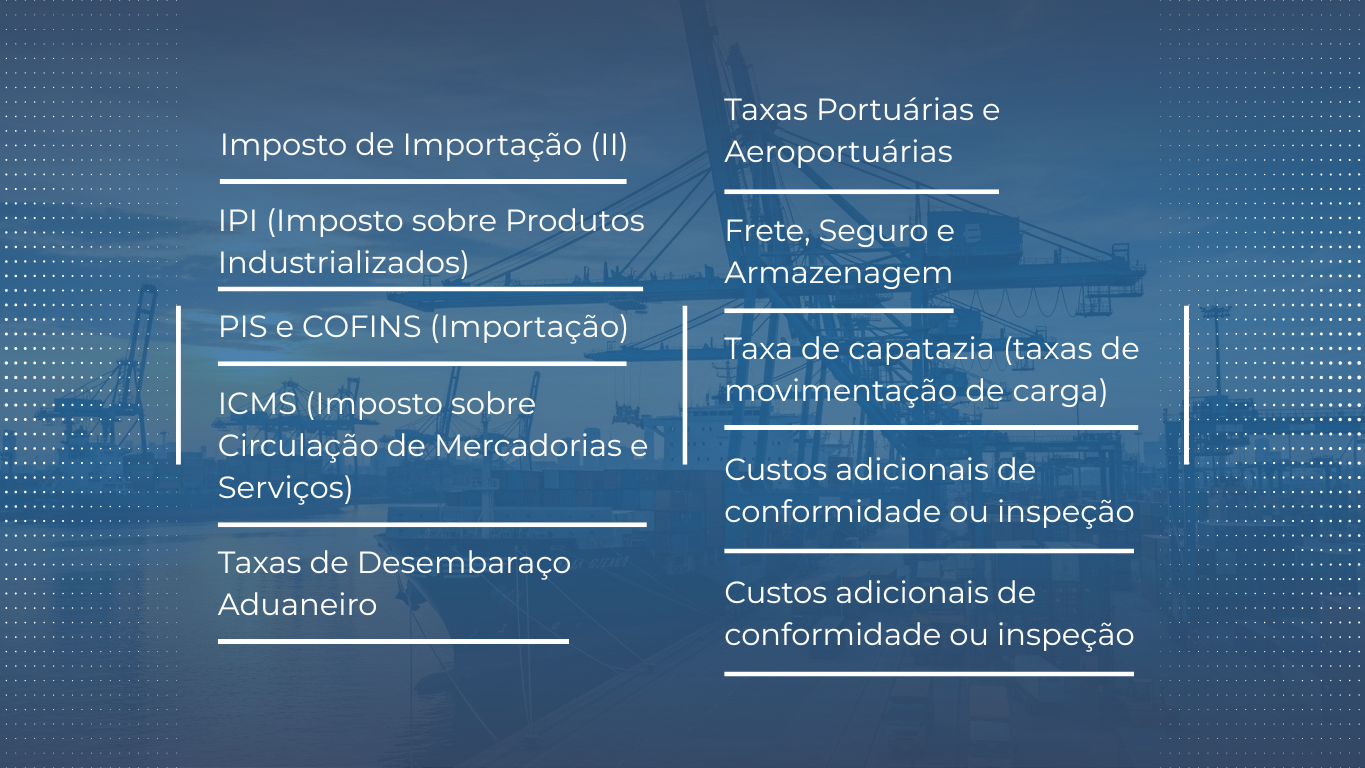

Importing into Brazil involves multiple taxes and fees, which together make importing relatively expensive. Below is an overview of the main cost components in 2026, explained in simple terms:

- Import Duty (II): A tariff on imported goods, applied to the CIF value (cost, insurance, and freight). The duty rate depends on the product’s classification (NCM/HS code) and typically ranges from 0% up to 20% or more. It is charged during customs clearance on the shipment’s declared value.

- IPI (Industrialized Products Tax): A federal excise tax on manufactured goods. For imports, IPI is charged at customs on the CIF value plus import duty. Rates vary (often 0–15%) depending on the product’s category (essential goods often low or 0%, luxury goods higher). IPI paid can be recovered as a credit if you are a company reselling the goods, since it’s a value-added type tax.

- PIS and COFINS (Import): These are federal social contribution taxes for social security and healthcare. On imports, PIS/COFINS are charged together (commonly a total of 9.25%) on the customs value. They are cumulative – calculated after adding import duty (and in some cases IPI) to the base. Like IPI, PIS/COFINS on imports can later generate credits to offset output PIS/COFINS on sales, but they still affect upfront cash outlay.

- ICMS (Merchandise and Services Circulation Tax): A state-level value-added tax. ICMS on imports is typically 17–19% (rate varies by state) and is applied on top of the sum of CIF value + duty + IPI + PIS/COFINS. In other words, it’s a tax on nearly the whole landed cost (including other taxes). Although paid at import, ICMS can often be credited back when the imported product is sold domestically (since it’s a value-added tax ultimately paid by the end consumer). Even so, it significantly impacts cash flow because it must be paid upfront to clear customs.

- Customs Clearance Fees: Importers face various clearance fees. Brazil charges a SISCOMEX fee (a fixed fee for processing the import declaration) and often a customs brokerage fee if using a broker. There may also be a contribution to the customs brokers’ union and fees for handling paperwork. These are typically fixed or modest amounts (e.g. a few hundred reais or dollars in total), but they add to the cost.

- Port and Airport Charges: When goods arrive, ports and airports impose handling and terminal fees. This includes “capatazia”, which refers to cargo handling charges for unloading and moving goods within the port terminal. There are also terminal handling charges (THC) and storage fees if your container or cargo stays in a bonded warehouse. These charges depend on the volume/weight of goods and time spent; delays in clearance can increase storage costs.

- Freight, Insurance and Storage: The cost of international freight and insurance is part of the import cost (and as noted, import duty and taxes are calculated on CIF, which includes these). Additionally, domestic transportation from the port to your warehouse is another cost. Storage or warehousing fees may accrue if goods are stored while awaiting clearance or distribution.

- “Capatazia” (Cargo Handling Fees): Specifically in Brazilian ports, capatazia fees are charged for physically handling cargo – e.g. crane operations, labor to move containers. This is usually included in the port costs but worth noting as a distinct item. It can be charged per tonne or per container.

- Additional Compliance or Inspection Costs: Depending on the nature of the goods, there could be extra costs for inspections or licenses. For example, imports of health-related products might require ANVISA (Health Authority) inspections/authorizations, and agricultural goods might need Agriculture Ministry (MAPA) inspections – these agencies may charge fees for issuing import permits or conducting inspections. Also, if goods require an import license before shipping, there might be fees associated with obtaining those licenses. While these costs are not huge in percentage terms, failure to comply can lead to penalties – which are an avoidable cost if you plan well.

Each of these components adds up. Import taxes in Brazil are often calculated in a cascading way, meaning one tax forms part of the base for the next. For instance, ICMS is calculated on a base that includes the other taxes and even the ICMS itself (a gross-up factor), making the effective impact higher than the nominal rate. It’s easy to see how a product’s cost can increase by 50% or more after all import duties, taxes and fees are applied.

What’s New in 2026

The year 2026 brings significant new factors that will impact the cost of importing into Brazil. Both regulatory changes and external conditions are altering the landscape:

- Tax Reform and New Tax Calculation: Brazil’s indirect tax reform begins its transition phase in 2026. While the classic import taxes (II, IPI, PIS/COFINS, ICMS) still apply in 2026, the groundwork is being laid for the new dual VAT system. A new federal tax, CBS (Contribuição sobre Bens e Serviços), and a state-level IBS (Imposto sobre Bens e Serviços) will slowly replace PIS, Cofins, IPI, ICMS and ISS between 2026 and 2032. In 2026, this means companies may start reporting under both systems in a pilot phase – for example, CBS at a very low rate of 0.9% and IBS at 0.1% might be applied on transactions for testing, while the existing taxes remain in force. Practically, importers should be aware that tax calculation methods might change. The reform aims to simplify and eliminate cascading taxes in the long run, but during the transition there could be complexity as old and new taxes coexist. It’s crucial to stay updated on how, for instance, PIS/COFINS on imports might evolve into CBS, and ICMS into IBS, affecting your pricing and tax credit recovery process.

- Changes in Tariffs or Exemptions: Keep an eye on tariff schedules and trade agreements in 2026. Brazil (as part of Mercosur) could adjust certain import duty rates or exceptions. One notable change is in the State of São Paulo: effective January 1, 2026, São Paulo will eliminate the upfront ICMS tax substitution (ICMS-ST) for hundreds of products. Under the old system, importers or manufacturers paid ICMS for the entire supply chain in advance (a heavy upfront cost); now those products will be taxed gradually at each sale stage. This aligns with the reform’s goal of ending such advance tax collection. For importers, it means lower initial tax outlays for those goods (though subsequent distributors will pay ICMS on their sales). Other states may implement similar changes. Also, the federal government sometimes updates Ex-tarifário lists (temporary import duty exemptions for certain machinery/tech not made locally) – new approvals or extensions in 2026 could reduce or zero-out import duty on qualifying capital goods.

- New Digital Customs Systems: Brazil is modernizing its customs clearance process. By 2024, the government launched the Portal Único de Comércio Exterior (Single Foreign Trade Portal) and its new DUIMP system (Declaração Única de Importação). In 2026, all importers are expected to be using this new system, which replaces the old Siscomex import declaration. The DUIMP allows integration of licensing, health agency approvals, and customs procedures into one online platform, streamlining the process. Government agencies like customs and ANVISA can now access import documents in real time, speeding up decisions – ANVISA has reported being able to clear certain imports in minutes under the new system. For companies, this digital shift means faster clearance (potentially lower storage costs) and a need to ensure your compliance data (invoices, classifications, licenses) is in order for electronic submission. There may be initial adaptation costs (upgrading systems, training staff), but over time digital processing should reduce delays and unpredictability in clearance, indirectly saving on port fees and storage charges.

- Global Logistics and Supply Chain Costs: The global shipping environment remains a wild card for 2026. Recent years have seen dramatic swings in freight costs – for example, disruptions in 2024 (like the Suez Canal or Panama Canal issues) caused freight rates to skyrocket. By late 2025, ocean freight rates have come down from pandemic highs but are still above pre-2020 norms and volatile. This means importers must budget for possible higher logistics costs if another disruption occurs. High fuel prices or container shortages can quickly increase shipping and insurance costs, which not only raise the CIF value (and thus all taxes), but also squeeze margins. Additionally, global supply chain delays can mean longer transit and more warehousing costs. In 2026, while the worst of the pandemic-era logistics crunch has eased, prudent companies will factor in a buffer for transportation and supply chain disruptions in their cost calculations.

- Currency Volatility: The exchange rate of the Brazilian Real (BRL) to major currencies (USD, EUR) is a pivotal factor in import costs. All taxes and duties in Brazil are calculated in BRL. If the Real depreciates in 2026, importing becomes more expensive in local currency terms – e.g. a $100,000 shipment costs R$500,000 at an exchange of 5 BRL/USD, but R$600,000 if the rate moves to 6 BRL/USD. That difference increases the base for import duty and taxes. Currency swings can thus significantly impact your landed cost. Importers should watch the forex trends and consider hedging large purchases. A stronger dollar/euro means Brazilian importers need more reais to buy the same goods, possibly leading to higher retail prices to maintain margins. Conversely, if the Real strengthens, tax amounts in BRL might drop, but relying on that is risky. In short, exchange rate risk is an integral part of import cost planning in 2026.

- Documentation, Compliance and Licensing Adjustments: Regulations evolve continuously. In 2026, there may be adjustments in import licensing requirements (for certain products, authorities might add or remove the need for special licenses). The push for compliance is increasing – Brazil has adopted systems like the Authorized Economic Operator (AEO) program (known locally as OEA), which rewards low-risk importers with faster clearance. Companies investing in compliance may gain cost advantages (less inspections, fewer delays). Also, Brazil is enhancing enforcement of correct NCM classification and valuation; misclassification can lead to fines or rejections. Thus, proper documentation and compliance aren’t new costs per se, but failing to comply can result in hefty penalties or storage fees in 2026’s stricter environment. Budget for any new inspection fees or certifications that might be required (for example, new health and safety standards for certain imports).

- Tax Credits and Exemptions Evolution: As tax rules change, so do opportunities for credits or exemptions. The tax reform includes mechanisms to ensure businesses can credit taxes on inputs more fully (to avoid cascading). In 2026, importers should review how they can utilize existing credits – e.g. ICMS paid at import can offset ICMS on sales, PIS/COFINS on imports can offset domestic PIS/COFINS. Also, watch for any regional incentives. Some states offer reductions in ICMS for certain industries or have free trade zones (like Manaus) with special regimes. The Manaus Free Trade Zone, for example, traditionally gives exemption from IPI and reduced import duties for approved operations – check if any rules there change in 2026. At the federal level, drawback (tax suspension for import inputs used in exports) might be expanded (recent laws even allowed some service costs to be included in drawback exemptions). Keeping track of these can help companies legally avoid unnecessary costs when the conditions fit.

Practical Impacts for Foreign Companies

With these changes in play, foreign companies importing into Brazil will feel the impact in several practical ways. It’s not just about paying a different tax rate – the ripple effects touch pricing, cash flow, and operations:

- Pricing Strategy: Higher or new import costs might force companies to adjust their pricing. If taxes or fees increase the landed cost, importers either pass that on as higher prices to Brazilian customers or absorb it in their margins. Conversely, any cost reductions (say, removal of a tax substitution in São Paulo) could give room to lower prices or out-compete others. Example: A foreign company importing machinery valued at $100,000 might currently face around $68,000 in combined taxes and charges, leading to a final landed cost of ~$168,000. If 2026 changes reduce some tax (imagine an ex-tarifário dropping the import duty from 14% to 0%), that same machine’s cost could drop by over $15,000, allowing the importer to offer a better price or enjoy higher profit per unit.

- Cash Flow and Working Capital: Import taxes in Brazil are paid upfront to clear goods. This means companies need significant cash on hand. If 2026 introduces a new fee or delays tax recovery, it can pinch cash flow. For instance, if CBS (the new tax) is collected alongside existing PIS/COFINS for a period, that’s an extra outlay until credits adjust. Companies will need to plan for possibly overlapping tax payments during the reform transition. On the positive side, changes like the removal of ICMS-ST in SP mean some importers won’t have to pay months’ worth of taxes upfront for the whole distribution chain – freeing up cash, though they’ll collect and remit taxes later on sales. It’s a timing shift that improves cash flow at import stage. Smart importers will update their cash flow forecasts for 2026 to account for these timing differences.

- Supply Chain Planning: The potential for logistics disruptions or changes in customs procedures means companies should build more resilience in their supply chain. For example, with the new DUIMP system, clearance may become faster on average, but during the rollout in 2026, any technical hiccups could cause delays. Companies might avoid cutting it too close with just-in-time inventory until they are confident in the new system’s stability. Also, given currency volatility and freight cost swings, importers might choose to advance purchases (import more before anticipated tax hikes or to hedge against currency moves) or diversify their freight routes to avoid hotspots (e.g. using alternative ports if one port gets congested). All these strategic moves can mitigate cost impacts, but require planning. Example: If you know global container rates are rising, securing an annual contract rate with carriers can lock in lower shipping costs – potentially saving, say, $2,000 on a $10,000 freight bill, which in turn saves you $500 in import duty (if 5% duty) and further taxes on that amount.

- Inventory Costs: Changes in import costs influence how much inventory companies can afford to hold. Higher import taxes/duties act like an immediate cost of goods sold, tying up more money in inventory value. If 2026 brings higher costs, some firms may reduce inventory levels to avoid cash sitting in warehoused stock (since each unit now costs more). Others might increase inventory before a tax change – for instance, importing extra stock in 2025 if they expect a tax increase in 2026. However, carrying more inventory has its own costs (storage, insurance, capital cost). Striking the balance is key. Also, with potentially faster customs clearance via DUIMP, the pipeline inventory (goods in transit or awaiting clearance) might shrink, which is beneficial. Companies should monitor clearance times in 2026 – if goods start clearing in days instead of weeks, you might not need as much safety stock, thereby cutting inventory costs.

- Tax Compliance and Audits: A more complex transitional tax system in 2026 (old and new taxes) could raise the compliance burden. Companies will spend more on accounting resources or software to ensure correct tax calculation on imports. Expect possibly higher costs for training staff or hiring consultants to navigate the reform. At the same time, Brazil is known for strict tax audits – mistakes in import declarations or tax payments can trigger fines. With new rules, the chance of mistakes goes up, so companies must invest in compliance now to avoid costly penalties later. Using updated software or hiring local tax experts may be an upfront expense, but it prevents far larger costs from errors or disputes. Many companies anticipate increased workloads and system updates due to the reform, which are short-term costs to achieve long-term simplification.

- Profit Margins: All the above factors funnel into your bottom line. If total import costs go up in 2026, profit margins shrink unless prices are raised or efficiencies found. Foreign companies selling in Brazil might see margins squeezed if they cannot fully pass on cost increases due to market competition. For example, imagine a product that used to cost R$1,000 landed and sold for R$1,200 (a 20% margin). If new taxes push landed cost to R$1,100, that same price now gives only ~9% margin unless adjusted. Companies will need to revisit their margin calculations product by product. In some cases, it may make certain low-margin imports no longer viable unless re-priced. Conversely, any cost savings from 2026 changes (like a tax exemption) could improve margins or be reinvested in market price competitiveness. The key is to continuously update cost sheets and profit analyses as the new rules take effect.

Real-World Example (Easy Math): Let’s say a U.S. exporter sells a piece of equipment to Brazil for $50,000 FOB. The freight and insurance add $5,000, so CIF is $55,000. Suppose the import duty is 10% = $5,500. IPI is 5% on (55k+5.5k) ≈ $3,025. PIS/COFINS 9.25% on (55k+5.5k) ≈ $5,625. ICMS 18% applied on the cumulative base (~ includes all above) roughly comes to an effective $12,000 (approx). Plus say $2,000 in various fees. The landed cost would be around $55k + $5.5k + $3k + $5.6k + $12k + $2k = $83,100 (in USD terms). That’s a 66% increase over the FOB price. If in 2026 the company can use an ex-tarifário to eliminate the 10% duty (saving $5,500) and São Paulo no longer requires upfront ICMS-ST (saving perhaps a few thousand more in immediate cost), the landed cost might drop to maybe ~$75,000. This improved scenario could mean the difference between a product being too expensive for the market versus competitively priced. Thus, understanding and leveraging the 2026 changes directly affects the company’s success in Brazil.

How to Reduce Import Costs in Brazil

Even with many unavoidable taxes, foreign companies can take steps to reduce the landed cost of imports into Brazil or at least mitigate the financial impact. Here are best practices to manage or lower import costs in 2026:

- Strategic Tax Planning: Good planning can prevent unnecessary costs. Work with Brazilian tax specialists to map out all applicable taxes and see where you can recover credits. Ensure you take advantage of credits for IPI, PIS/COFINS, and ICMS on imports – these can offset taxes on your sales so that, in effect, those import taxes aren’t a true cost in the long run (except if you sell to end consumers who can’t pass it on). Also stay informed about the tax reform rollout – if CBS will replace PIS/COFINS, understand how the credit system works so you don’t lose credits during the transition. Planning your imports’ timing can help too: for instance, if a tax rate will drop or an exemption will start soon (like a tariff reduction scheduled), you might postpone a shipment to arrive when the lower rate applies.

- Review NCM Classification: The import duty rate and many taxes depend on the NCM (Mercosur Common Nomenclature) code of your product. Misclassification can mean paying higher duty or missing out on an exemption. Ensure your product is classified under the correct code that attracts the lowest lawful duty. Sometimes a product might fit into two categories – classify it under the one with a favorable rate if it’s justifiable and compliant. Do not falsify classifications (penalties are severe), but do research if your item has any special classification rulings or is eligible for any tariff code that has a reduced rate (e.g. certain green technologies or pharmaceuticals might have 0% duty lines). Engaging a customs consultant or using advance rulings from authorities can confirm the best classification. This can save a lot; for example, shifting to an NCM with 2% duty from one with 10% duty on a $100,000 import saves $8,000 right off the bat.

- Negotiate Incoterms and Logistics: How you structure your purchase agreements can affect costs. Incoterms determine who pays for freight, insurance, and import clearance. Foreign exporters and Brazilian importers should carefully choose terms like FOB, CFR, CIF, DAP, etc. For a Brazilian importer, FOB (Free on Board) can be beneficial because it gives control over the international freight – you can shop around for the best shipping rates or use your own bulk rates. Lower freight cost means a lower CIF, which means lower duties and taxes (since they’re calculated on CIF). Conversely, if an exporter can get a much cheaper shipping rate than you, a CIF deal could lower your cost – the key is to compare. Also, negotiate how handling charges are dealt with: sometimes splitting shipments or using a different port with lower fees can reduce costs. For instance, importing via a slightly more distant port that has lower port fees might save money overall if trucking internally is cheaper than paying a premium at a congested port. In 2026’s environment, be flexible and optimize your logistics strategy for cost – including consolidating shipments (to save on minimum fees) or timing imports to avoid peak seasons (when freight rates and port warehouses are costlier).

- Use Special Customs Regimes: Brazil offers several special regimes that can significantly reduce or defer import taxes:

- Ex-Tarifário: As mentioned, this regime allows temporary reduction of import duty to 0% for qualifying capital goods and technology equipment that have no local equivalent production. If you are investing in machinery, check if an ex-tariff concession exists or can be requested for your equipment. It can save the entire import duty amount, which is a huge cost reduction. For example, if your machine’s NCM normally has 14% duty, an ex-tarifário approval saves that 14%. The process requires a Brazilian entity to apply with technical details, and it takes a few months, but the savings on a big import are well worth it.

- Drawback Regime: If your business model involves importing raw materials or components to manufacture in Brazil for export, the Drawback program can eliminate or refund the import taxes on those inputs. Under Drawback Suspension, you don’t pay II, IPI, PIS/COFINS, or ICMS on approved imported inputs that will be used for export production. This can make a dramatic difference in costs for export-oriented manufacturers (essentially importing tax-free). In 2026, drawback has been expanded to even cover some services related to exports, further lowering costs. Foreign companies setting up manufacturing in Brazil should leverage this to stay competitive globally.

- RECOF and RECOF-Sped: These are special regimes for authorized companies that allow stocking imported goods under tax suspension for use in production or for certain re-export scenarios. They are complex to obtain (generally for high-volume importers/exporters with robust controls), but effectively you warehouse goods without paying duties until they leave the regime (for local sale, at which point taxes become due, or for export, then exempt). It’s like having a bonded manufacturing warehouse – great for cash flow if you qualify.

- Temporary Admission (Admissão Temporária): If you are importing goods temporarily (for a trade show, for repair, or leasing equipment), there are regimes that suspend or reduce taxes as long as the item is exported again within a set period. Make sure to use these when applicable rather than doing a normal import which would incur full taxes on something not staying in Brazil.

- Free Trade Zones and Incentives: If your operations can be in or route through a Brazilian Free Trade Zone (like Manaus), explore the local incentives. Manaus, for example, offers exemption of import duty and IPI for approved industries operating there, plus reduced ICMS. While that’s very location-specific, it can be a strategy to import into a FTZ, do light processing, and then distribute in Brazil with some tax benefits (though ICMS often gets charged when moving out of the zone).

- Strengthen Compliance to Avoid Penalties: Brazilian customs and tax authorities enforce regulations rigorously. Mistakes in documentation or non-compliance can lead to fines, storage delays, or even seizure of goods – all of which are avoidable costs. Invest in accurate documentation: ensure commercial invoices, packing lists, and certificates (origin, sanitary, etc.) are correct and complete. Adhere to Brazilian import licensing requirements (use the new systems to obtain licenses or permits in advance). By being compliant, you will avoid costly surprises like a fine for mis-declaring value or a penalty for late filing. Also, consider AEO/OEA certification if you are a frequent importer – being an Authorized Economic Operator can expedite your shipments and reduce inspections, indirectly cutting time-related costs. Essentially, compliance is cost prevention. Paying a skilled customs broker or trade compliance expert is worth it if it prevents a cargo from sitting at port incurring storage for weeks due to a paperwork issue. In 2026, with new rules coming in, ensure your team is up-to-date and perhaps run audits on your import processes to catch any errors proactively.

By combining these practices – savvy tax planning, correct classification, optimized logistics, use of regimes, and top-notch compliance – foreign companies can significantly reduce the landed cost of their imports into Brazil. For example, a company that correctly classifies products and secures an ex-tarifário might save tens of thousands of dollars on a shipment; using the drawback could enable an exporter to import components tax-free, making their final product much cheaper to produce. Every percentage point saved in taxes or fees is directly added to your margin or passed on as a better price to win in the market.

FAQ: Common Questions on Brazil’s Import Costs

Q1: Why is importing to Brazil so expensive?

A: Importing to Brazil is often expensive because of the cumulative taxes and fees levied at the border. Brazil’s import tax structure includes import duties, federal taxes like IPI and PIS/COFINS, and state ICMS, which are applied in a cascading manner (tax-on-tax). These can add up to 40-60% (or more) of the product’s value in many cases. Additionally, operational costs – such as high port fees, mandatory handling charges (capatazia), and logistics costs – further increase the landed cost. Brazil historically implemented these high import taxes to protect local industry and generate revenue. While many of these taxes can later be recovered as credits by companies (if they sell domestically and pay those taxes forward), the upfront cash outlay is significant. Complex compliance requirements and occasional delays can introduce extra costs (like storage and demurrage fees), making the import process costlier than in many other countries. In summary, multiple layers of taxation and logistics charges drive up the expense of importing into Brazil.

Q2: What taxes apply to imports in Brazil?

A: The main taxes on imports in Brazil (as of 2026) are:

- Import Duty (II): A tariff on the good’s value (varies by product, e.g. 0% for some capital goods up to 20% or more for consumer goods).

- IPI (Tax on Industrialized Products): A federal tax on manufactured goods, applied at import; rate depends on product category (often 5–15%).

- PIS and COFINS (Import): Federal social contributions, totaling generally 9.25%, applied on the customs value plus duty.

- ICMS: A state tax on goods circulation, around 17% (varies by state) on the CIF value plus all the above taxes.

- In addition, there are smaller fees: e.g. SISCOMEX fee (for customs processing), AFRMM (a 25% tax on ocean freight for the Merchant Marine Fund, if importing by sea), customs broker fees, handling and storage fees, etc. These are not “taxes” per se but official charges that apply to many imports.

Brazil is undergoing a tax reform, so starting in 2026-2027, PIS and COFINS will gradually be phased out and replaced by a new tax called CBS, and ICMS (along with a municipal service tax ISS) will be replaced by IBS, forming a dual VAT system. During the transition, the old taxes still apply, but once fully implemented by 2032, imports will be subject to CBS, IBS, and an excise tax (Selective Tax) instead – all aimed to simplify the current array of taxes. But in 2026, importers still face the traditional set of taxes listed above.

Q3: Does currency exchange rate impact import cost?

A: Yes, absolutely. The exchange rate between the Brazilian Real (BRL) and foreign currencies (USD, EUR, etc.) has a direct impact on import costs. All duties and taxes are calculated in BRL on the CIF value converted to local currency. If the Real weakens (depreciates), the same dollar price translates to more reais, increasing the tax base. For example, a machine priced at $10,000 would be ~R$50,000 if the rate is 5 BRL/USD. If the real slips to 6 BRL/USD, that’s R$60,000. Import duty, IPI, PIS/COFINS, and ICMS will all be calculated on R$60,000 instead of R$50,000 – meaning higher amounts due. A rough calculation: at 30% total import taxes, that $10,000 machine would incur R$18,000 in taxes at the 5 BRL rate, but R$21,600 at the 6 BRL rate. That’s a significant difference purely from exchange fluctuation.

Conversely, if the Real strengthens (appreciates), imports become cheaper in local terms, and you pay less tax for the same foreign price. However, currency movements are hard to predict, so importers often use hedging strategies or negotiate contracts in a way to mitigate risk. It’s also why some foreign suppliers may agree to invoice in BRL – shifting exchange risk to themselves – but usually at a premium. Overall, a volatile exchange rate means volatile import costs, so finance teams should monitor FX rates closely and possibly secure forward contracts for large purchases to gain cost certainty.

Q4: How can companies reduce the landed cost in Brazil?

A: Companies can employ several strategies to reduce landed costs:

- Optimize import planning: Consolidate shipments to achieve economies of scale (a full container will spread fixed costs better than many small shipments). Avoid unnecessary air freight (very costly) by planning ocean shipments well in advance.

- Leverage tax incentives: Use regimes like Ex-tarifário to cut import duty to 0% on approved goods. If you export from Brazil, use Drawback to import inputs tax-free. See if your goods qualify for any special exemptions (e.g. certain green technology or pharma inputs sometimes have zero duty).

- Accurate product valuation: Declare the correct transactional value, but utilize allowed deductions. For instance, some costs like post-import inland freight are not part of CIF – ensure they’re not mistakenly taxed. Use transfer pricing mechanisms carefully (for related-party transactions) to avoid overvaluing your imports.

- Incoterm negotiation: Aim for terms that give you control over freight and insurance – often FOB or FCA, so you can manage those costs. By lowering CIF, you lower duties and taxes. Just ensure you have the capability to handle logistics effectively if taking on that responsibility.

- Efficiency at clearance: Ensure all paperwork is correct to avoid delays. Every extra day a container sits at port, you rack up storage and demurrage fees. Pre-clear cargo whenever possible (Brazil allows some advance customs clearance processes). Also, consider using ports or airports known for efficiency even if they are slightly farther, as delays = money.

- Local partnerships: Work with a reliable customs broker and logistics provider. They might have duty drawback programs or bonded warehousing options that let you defer taxes. A good broker can also classify your goods favorably and navigate the bureaucracy swiftly.

- Monitor changes: Finally, stay informed about regulatory changes (like the tax reform rollout, new free trade agreements that lower tariffs, etc.). Adapting quickly to a change (for example, if a tariff is reduced on your product, or a new bilateral trade agreement cuts duty by half) can save you money that slower competitors might still be losing.

In essence, reducing landed cost in Brazil comes down to planning, using legal incentives, and running a tight ship on logistics and compliance. Companies that invest effort in these areas often find they can trim a good portion of the Brazil cost “penalty” and compete more effectively.

Conclusion and Call to Action

Importing into Brazil in 2026 will come with new costs and new opportunities. The country is at the start of a transformative period: a tax reform aiming to simplify the system, digital innovations speeding up customs, and shifting economic conditions. Foreign businesses that proactively adjust to these changes – revisiting their pricing, ensuring compliance, and leveraging cost-saving measures – will turn what could be a challenge into a competitive advantage. It’s all about strategic planning: understanding the updated tax structure, preparing for currency and logistics fluctuations, and using every available tool to manage costs.

As you navigate Brazil’s import landscape, remember you don’t have to do it alone. My Business Brazil is here to provide guidance, up-to-date insights, and connect you with trusted local partners. Whether you need clarity on a new import rule, help with tax planning, or introductions to reliable customs brokers and logistics providers, we’ve got you covered. Import costs may be evolving, but with the right knowledge and support, your company can thrive in 2026 and beyond.

Ready to tackle Brazil’s import market? Contact My Business Brazil for expert assistance and turn these changes into opportunities for growth. We’re committed to helping foreign investors and importers succeed in Brazil’s dynamic business environment – every step of the way.

0 Comments