Quick answer

Foreign companies operating in Brazil should manage compliance through a monthly, annual and event-based calendar. The core routines usually include payroll and eSocial, FGTS Digital, EFD-Reinf, DCTFWeb, PIS/COFINS, IRRF, ISS or ICMS, ECD, ECF, annual corporate approvals and Central Bank SCE-IED declarations when the Brazilian entity receives foreign direct investment. The exact calendar depends on the company’s tax regime, state, municipality, industry, payroll, foreign capital position and cross-border transactions.

Why foreign companies need a Brazilian compliance calendar

Brazilian compliance is not a single annual tax return. It is a recurring system of accounting, payroll, tax, corporate, labor, foreign capital and digital reporting obligations. For foreign companies, the risk is not only missing one deadline. The bigger risk is that one incorrect filing can create inconsistencies across several systems.

Receita Federal, eSocial, FGTS Digital, municipal systems, state tax authorities, the Board of Trade and the Central Bank of Brazil all collect different pieces of information. When payroll, invoices, accounting books, tax declarations and foreign capital records do not match, the company may face fines, blocked certificates, audit exposure or delays in dividends, capital movements and corporate transactions.

The safest approach is to run Brazil as a controlled monthly closing process. That means defining owners, deadlines, evidence, reconciliations, approvals and escalation rules before the first fiscal year becomes messy.

Executive compliance calendar

The table below summarizes the key timing logic. It is not a substitute for a customized tax agenda, but it gives foreign management teams a realistic operating map.

| Frequency | Main obligations | Typical timing | Foreign company note |

| Daily / event-based | Invoices, withholding tax triggers, imports, exports, foreign exchange, admissions, terminations, corporate changes | Event date | Must be monitored as transactions occur. |

| Monthly | Payroll, eSocial, FGTS Digital, DCTFWeb, EFD-Reinf, PIS/COFINS, IPI, IRRF, ISS/ICMS routines | Usually between days 15, 20, 25 and month-end, depending on obligation | Exact dates vary by tax, source system and business day rules. |

| Quarterly | IRPJ/CSLL for quarterly regimes; SCE-IED quarterly declaration for large foreign-invested companies | Quarter-end or fixed BCB periods | Applies only to certain companies. |

| By March 31 | SCE-IED annual or quinquennial foreign capital declaration where applicable | Jan 1 to Mar 31 | Thresholds depend on assets and year type. |

| By April 30 | Annual quotaholders/shareholders meeting for approval of accounts, where fiscal year ends Dec 31 | First four months after fiscal year-end | Corporate law routine, not a tax filing. |

| By last business day of June | ECD – Digital Accounting Bookkeeping | Year following the calendar year | Normal situations. Special events have their own rules. |

| By last business day of July | ECF – Digital Tax Accounting Bookkeeping | Year following the calendar year | Most non-Simples legal entities are subject to ECF. |

| November / December | 13th salary installments and year-end payroll provisions | First installment generally by Nov 30; second by Dec 20 | Payroll cash-flow planning is essential. |

Monthly compliance routines

Monthly compliance is where most mistakes happen. Foreign headquarters often see Brazil’s annual obligations, but the actual risk lives in monthly closing: invoices, payroll, withholdings, indirect taxes, digital bookkeeping and payment guides.

| Obligation | What it covers | Calendar logic |

| eSocial payroll events | Payroll, admissions, leaves, vacation, terminations and labor events | Admissions must be reported by the day before work starts; payroll events follow the monthly closing routine. |

| FGTS Digital | Monthly FGTS deposits | Since FGTS Digital, the monthly FGTS due date is generally the 20th of the following month, with anticipation if the date falls on a non-business day. |

| EFD-Reinf | Withholdings and other tax information not covered by payroll eSocial | Commonly due on the 15th of the month following the reference period. |

| EFD-Contribuicoes | PIS/COFINS digital bookkeeping | Commonly shown in the Receita Federal agenda on day 15 for the relevant reference period. |

| DCTFWeb / tax confession and DARF generation | Confession and payment flow for federal taxes integrated from eSocial, Reinf and MIT | Check the current Receita Federal agenda; dates changed in recent years and depend on the tax/category. |

| PIS/COFINS / IPI / IRRF / IOF | Federal tax payments and withholdings | Usually concentrated around days 20, 25 or month-end depending on tax and period. |

| ISS / ICMS | Municipal service tax and state VAT-like tax | Deadlines vary by municipality/state and taxpayer profile. |

Annual accounting and tax filings

ECD – Digital Accounting Bookkeeping

ECD is the digital accounting bookkeeping file. For normal situations, the Receita Federal’s SPED FAQ states that the filing deadline is the last business day of June of the year following the calendar year to which the bookkeeping relates. Special events such as merger, spin-off, incorporation or liquidation follow specific deadlines.

ECF – Digital Tax Accounting Bookkeeping

ECF replaced the old DIPJ and contains the tax accounting information used for IRPJ and CSLL. The SPED guidance states that the normal deadline is the last business day of July of the year following the relevant calendar year. ECF is generally required for legal entities taxed under Lucro Real, Lucro Presumido or Lucro Arbitrado, as well as immune and exempt entities, with exceptions such as Simples Nacional companies.

Financial statements and annual corporate approval

Brazilian companies usually need annual approval of management accounts and financial statements within the first four months after the end of the fiscal year. For companies whose fiscal year ends on December 31, the approval meeting or resolution is normally held by April 30. The minutes may need to be filed with the Board of Trade, depending on the corporate type and situation.

Foreign capital and Central Bank obligations

Foreign-owned Brazilian companies must pay special attention to Central Bank reporting. The SCE-IED system is used for foreign direct investment information. The obligation is not limited to the initial capital contribution; periodic declarations may apply according to the company’s assets and the reporting year.

According to gov.br service guidance, periodic SCE-IED obligations include: quarterly declarations for companies with total assets equal to or above BRL 300 million on the quarterly base date; annual declarations for companies with total assets equal to or above BRL 100 million on December 31; and quinquennial declarations, in years ending in 0 or 5, for companies with total assets equal to or above BRL 100 thousand on December 31. The declaratory period for annual and quinquennial filings is generally January 1 to March 31 of the following year.

Foreign capital warning

Foreign companies should reconcile SCE-IED information with corporate records, accounting books, capital contributions, dividends, interest on equity, loans, foreign exchange contracts and financial statements. A mismatch can delay future capital movements or create regulatory exposure.

Payroll and labor calendar

Payroll compliance in Brazil has its own rhythm. Admissions must be reported before the employee starts working. Monthly payroll data feeds eSocial. FGTS is calculated through FGTS Digital. INSS, IRRF and other amounts flow through federal systems. Vacation, leaves, terminations and occupational health events also have specific event deadlines.

- Admission: register the employee in eSocial by the day before the start of work.

- Monthly payroll: close salary, benefits, overtime, absences and deductions before submitting events.

- FGTS Digital: monthly FGTS is generally due by the 20th of the following month.

- Termination: calculate severance, FGTS termination amounts and eSocial events according to the termination type.

- 13th salary: plan cash flow for the two installments, usually by November 30 and December 20.

- Vacation: monitor acquisition and concession periods to avoid late vacation liabilities.

State and municipal compliance

Foreign companies should not rely only on the federal calendar. ICMS obligations are state-level and ISS obligations are municipal-level. Deadlines vary depending on the state, city, activity, tax regime, invoice model and special regimes. A company with branches or service delivery in multiple locations may need more than one local calendar.

This is especially relevant for importers, distributors, e-commerce, SaaS, technology services, consulting, logistics, manufacturers and companies issuing both product invoices and service invoices.

Event-based compliance triggers

- Opening a Brazilian entity, branch or establishment.

- Changing shareholders, administrators, address, corporate purpose or share capital.

- Receiving foreign investment or making capital reductions, dividends or interest on equity payments.

- Signing cross-border service, royalty, loan, cost sharing or technology agreements.

- Hiring, terminating or changing employee conditions.

- Importing or exporting goods or services.

- Starting operations in a new state or municipality.

- Mergers, spin-offs, incorporations, liquidation or other corporate reorganizations.

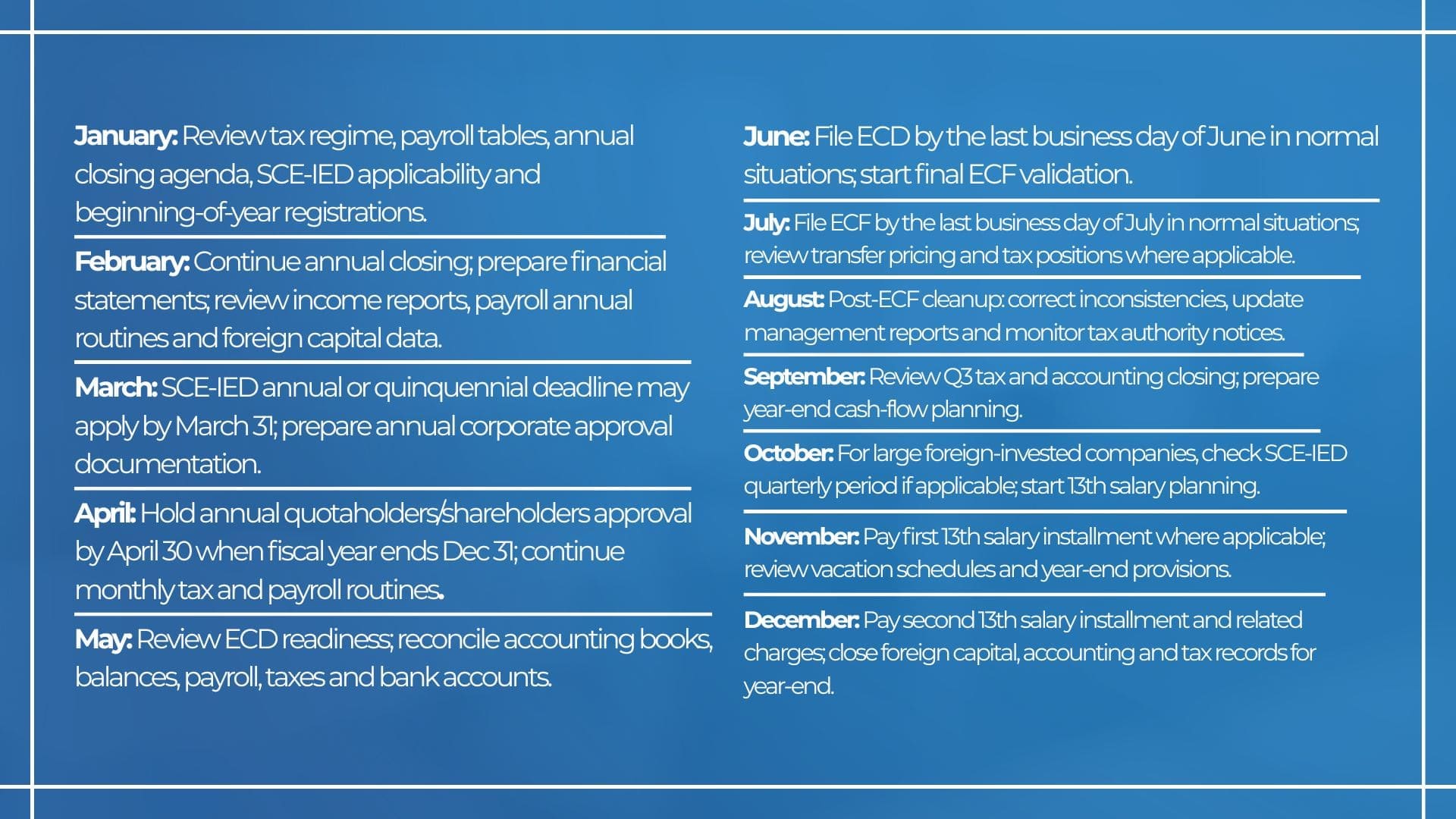

January to December operating map

How to build an internal Brazil compliance calendar

- Map the company’s tax regime, activities, states, municipalities, payroll profile and foreign capital position.

- Separate obligations into monthly, annual, quarterly and event-based categories.

- Assign an owner for each obligation: accounting, tax, payroll, legal, treasury or corporate secretarial.

- Define evidence: receipt, protocol, payment guide, reconciliation, approval email and accounting support.

- Create a closing checklist before filings are transmitted.

- Reconcile systems: ERP, accounting, payroll, eSocial, Reinf, DCTFWeb, SPED, banks and SCE-IED.

- Review the Receita Federal tax agenda monthly because deadlines and systems can change.

Common mistakes foreign companies make

- Treating Brazil as an annual tax-return country instead of a monthly compliance environment.

- Missing state and municipal obligations while focusing only on federal taxes.

- Failing to reconcile payroll, eSocial, FGTS Digital and accounting provisions.

- Preparing ECD and ECF too late, after accounting inconsistencies have accumulated.

- Ignoring SCE-IED deadlines for foreign capital because the finance team sees them as legal, not accounting.

- Changing corporate data without updating tax, payroll, banking and Central Bank records.

- Assuming that a global ERP calendar automatically captures Brazilian obligations.

Useful CLM Controller resources

These CLM Controller resources connect naturally with Brazil compliance calendar planning:

- Accounting outsourcing

- Tax outsourcing

- Payroll outsourcing

- Accounting tax consultancy

- Internationalization in 2026: accounting and tax challenges

- How to avoid tax risks in international operations

- CLM Controller English Blog

Conclusion

A Brazil compliance calendar is not just a list of dates. It is a control system for keeping accounting, tax, payroll, corporate and foreign capital information aligned. For foreign companies, this alignment is what protects the Brazilian operation from fines, blocked certificates, audit exposure and delays in strategic decisions.

The right calendar should be customized by tax regime, activity, location, payroll, foreign investment profile and cross-border transactions. Once built, it should be reviewed monthly, because Brazilian compliance is dynamic and system-driven.

| Need a Brazil compliance calendar for your company? CLM Controller helps foreign companies operating in Brazil manage accounting, tax, payroll, corporate and foreign capital routines with specialized outsourcing, tax consultancy, payroll support and management reporting. If your company needs a reliable Brazil compliance calendar, talk to CLM Controller and organize the operation before deadlines become liabilities. |

FAQ: Brazil compliance calendar for foreign companies

What are the main compliance obligations for foreign companies in Brazil?

The main routines are monthly payroll and tax filings, eSocial, FGTS Digital, EFD-Reinf, DCTFWeb, PIS/COFINS, IRRF, ISS or ICMS, ECD, ECF, corporate approvals and SCE-IED foreign capital declarations when applicable.

Is there one national tax calendar for all companies?

No. Receita Federal publishes a federal tax agenda, but companies also need state, municipal, payroll, corporate and Central Bank calendars.

When are ECD and ECF due?

In normal situations, ECD is due by the last business day of June and ECF by the last business day of July of the year following the calendar year. Special corporate events have specific deadlines.

Do all foreign-owned companies file SCE-IED declarations?

Not all periodic declarations apply to every company. Applicability depends on foreign direct investment status, total assets and whether the year is annual, quarterly or quinquennial for reporting purposes.

When is the annual corporate approval deadline?

For companies whose fiscal year ends on December 31, annual approval of accounts is usually held within the first four months of the following year, normally by April 30.

What is the biggest compliance risk for foreign companies in Brazil?

The biggest risk is system inconsistency: payroll, invoices, tax filings, accounting books, bank records and foreign capital declarations saying different things.

Sources consulted

- Receita Federal – 2026 tax agenda

- SPED – ECD FAQ deadline

- SPED – ECF guidance and deadline

- SPED – ECF FAQ deadline

- FGTS Digital – monthly due date

- eSocial FAQ – admission reporting

- Gov.br – SCE-IED foreign direct investment reporting

- Gov.br – Foreign capital census reporting

- CLM Controller – Accounting outsourcing

0 Comments