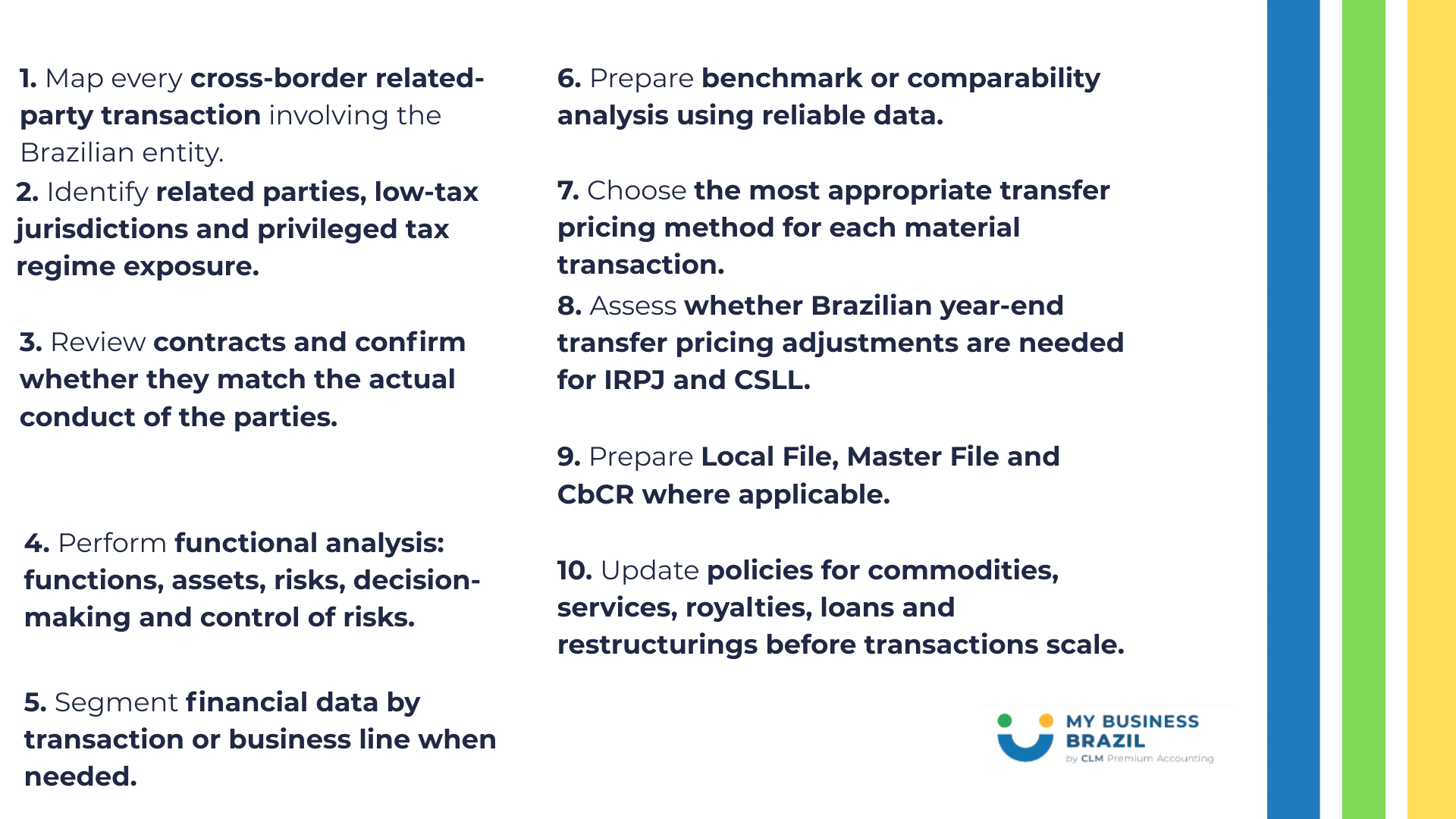

Quick answer

Brazil’s transfer pricing rules changed substantially with Law 14,596/2023 and Normative Instruction RFB 2,161/2023. Since 2024, multinational groups with Brazilian entities must apply an OECD-aligned arm’s length standard to controlled cross-border transactions that affect IRPJ and CSLL. The rules cover goods, services, intangibles, commodities, financial transactions, cost contribution arrangements and business restructurings. Multinationals must document the transaction, choose the most appropriate method, support comparability and prepare Local File, Master File and other reporting where applicable.

Why Brazil transfer pricing changed

For many years, Brazil used a transfer pricing system that was highly prescriptive and based on statutory formulas and fixed margins. That model was simpler in some situations, but it was also distant from the international standard used by most OECD-oriented tax administrations.

Law 14,596/2023 changed this framework by incorporating the arm’s length principle into Brazilian tax law. Normative Instruction RFB 2,161/2023 then regulated important parts of the new system. The new rules became mandatory from 2024, with an optional early adoption mechanism for 2023.

The practical effect is major: multinational groups can no longer rely on Brazil-only fixed margin logic. They need to analyze controlled transactions economically, compare them with independent market behavior and document why the prices, margins and terms used by the Brazilian company are arm’s length.

Who is subject to Brazil’s transfer pricing rules?

The rules apply to legal entities domiciled in Brazil that carry out controlled transactions with related parties abroad, and to other situations covered by Brazilian legislation, including transactions involving parties in low-tax jurisdictions or privileged tax regimes where applicable.

A multinational should pay attention when a Brazilian subsidiary, branch or permanent establishment buys, sells, licenses, borrows, lends, shares costs, receives services, provides services, transfers intangibles or enters into restructurings with group entities outside Brazil.

Common controlled transactions

- Import or export of products, inputs, finished goods and commodities.

- Provision or receipt of intragroup services.

- Royalties, licenses, technology, software and other intangible transactions.

- Intercompany loans, guarantees, cash pooling, treasury and other financial transactions.

- Cost contribution arrangements and cost sharing agreements.

- Business restructurings, transfers of functions, assets or risks.

- Transfers of shares, rights or other assets between related parties.

The arm’s length principle in practice

The arm’s length principle asks whether the terms and conditions of a controlled transaction are consistent with what independent parties would have agreed under comparable circumstances. This is not only a price test. It also covers functions performed, assets used, risks assumed, contractual terms, economic circumstances and business strategies.

For Brazilian taxpayers, this means that the transfer pricing file should explain the transaction from beginning to end: who does what, who owns or controls which assets, who bears which risks, how the price was set, which method was selected, what comparables were used and whether any adjustments are needed for IRPJ and CSLL.

Transfer pricing methods in Brazil

The Brazilian framework now uses OECD-style methods. The taxpayer must select the most appropriate method based on the controlled transaction and the reliability of available information.

| Method | What it does | Typical use |

| PIC / CUP | Compares the price or value of a controlled transaction with comparable uncontrolled transactions. | Often the preferred method when reliable comparable prices exist, especially for commodities. |

| PRL / Resale Price | Starts from the resale price to an independent party and subtracts an appropriate gross margin. | Useful for distributors and resale operations when reliable gross margins are available. |

| MCL / Cost Plus | Starts from direct and indirect costs and adds an arm’s length gross margin. | Useful for manufacturing or service arrangements where costs are reliable and comparable markups exist. |

| MLT / TNMM | Tests the net profit margin relative to an appropriate base such as sales, costs or assets. | Common for routine entities when gross margin data is less reliable. |

| MDL / Profit Split | Allocates combined profit according to each party’s contribution. | Relevant for highly integrated operations or transactions involving unique contributions by more than one party. |

| Other methods | Alternative methods may be used when they produce a more reliable arm’s length result. | Requires strong support and clear reasoning. |

Documentation requirements: Local File, Master File and CbCR

Documentation is one of the biggest practical changes for Brazilian entities of multinational groups. The taxpayer must be able to demonstrate that the controlled transactions comply with the arm’s length principle. Depending on the volume of controlled transactions, Local File and Master File obligations may apply.

| Transaction volume / file | Documentation implication |

| Below BRL 15 million in controlled transactions | Generally waived from Local File and Master File submission, but the taxpayer must still comply with the arm’s length principle and keep support for the pricing policy. |

| BRL 15 million to below BRL 500 million | Simplified Local File plus Master File requirements apply, according to the RFB framework. |

| BRL 500 million or more | Complete Local File and complete Master File requirements apply. |

| CbCR | Country-by-Country reporting may apply under the existing Brazilian BEPS Action 13 framework for qualifying multinational groups. |

Even when a formal file is waived because transaction volume is below a threshold, the taxpayer should not treat transfer pricing as irrelevant. The arm’s length principle still applies, and the company should keep enough support to explain the pricing policy if questioned.

Commodities: special attention for Brazilian groups

Commodities are especially important in Brazil because of the country’s role in agriculture, mining, energy and other export sectors. Under the new rules, the PIC method is generally appropriate when reliable independent quoted prices are available.

The pricing date or pricing period can be critical because commodity prices move quickly. Companies need to document the date agreed by the parties and maintain evidence that the pricing terms are consistent with arm’s length behavior. The Receita Federal has also issued guidance and updates on the Registro de Transacoes com Commodities (RTC), which became relevant from 2025.

Intragroup services and low value-added services

Intragroup services are common in multinational groups: management support, administrative services, finance, HR, IT, legal coordination, marketing support and shared services. Under the Brazilian rules, the company must first prove that a real service was provided and that it created or could reasonably create economic or commercial value for the recipient.

Brazil also introduced a simplified approach for low value-added intragroup services. In broad terms, qualifying support services may use a 5% cost-based margin: at least 5% when the Brazilian entity is the service provider and at most 5% when the provider is a related party abroad. However, not all services qualify. Core business services, R&D, manufacturing, sales, marketing, financial transactions and high-value intangible-related services generally require a fuller analysis.

Intangibles, royalties and DEMPE analysis

Intangible transactions are one of the areas where the new model can create the most significant impact. Multinationals must look beyond legal ownership and analyze who performs and controls the development, enhancement, maintenance, protection and exploitation of intangibles.

A Brazilian entity that contributes valuable functions to a brand, technology, software, customer relationship or know-how may need to be remunerated accordingly. Likewise, payments from Brazil for royalties or technology must be supported by actual benefits, contractual evidence and arm’s length pricing.

Financial transactions

The new transfer pricing system also requires economic analysis of financial transactions. Intercompany loans, guarantees, cash pooling and treasury arrangements should reflect the credit profile, currency, term, collateral, risks, market conditions and realistic alternatives of the parties.

This is a major shift for groups that previously treated Brazil intercompany financing mainly as a withholding tax, thin capitalization or foreign exchange issue. The pricing itself must now be supported under transfer pricing principles.

Business restructurings and cost contribution arrangements

Business restructurings can trigger transfer pricing questions when functions, assets, risks, contracts or profit potential are moved across borders. Examples include converting a full-risk distributor into a limited-risk distributor, centralizing procurement, transferring technology, moving decision-making abroad or changing the Brazilian entity’s role in the value chain.

Cost contribution arrangements also require careful documentation. The allocation key must reflect expected benefits, and participants’ contributions must be consistent with the value they receive or expect to receive.

Implementation checklist for multinationals in Brazil

| Practical recommendation Do not treat Brazil transfer pricing as an annual compliance file only. Multinationals should connect tax, accounting, legal, finance, supply chain and operations before prices are set. The strongest transfer pricing defense is built during the transaction, not after the fiscal year closes. |

Common mistakes to avoid

- Using old Brazil fixed-margin logic after the new arm’s length regime became mandatory.

- Preparing a global transfer pricing policy but failing to adapt it to Brazilian IRPJ and CSLL rules.

- Keeping contracts that do not reflect the real conduct, functions and risks of the parties.

- Ignoring services received from related parties abroad or failing to prove benefit.

- Assuming a 5% service margin applies without checking the low value-added service requirements.

- Not documenting commodity pricing dates and quoted-price evidence.

- Treating intercompany loans as purely legal or treasury matters without transfer pricing support.

- Waiting until the ECF deadline to collect data that should have been tracked during the year.

Useful CLM Controller resources

These CLM Controller materials connect naturally with transfer pricing, international operations and tax compliance:

- Accounting tax consultancy

- Tax consultancy and transfer pricing support

- Internationalization in 2026: accounting and tax challenges

- How to avoid tax risks in international operations

- Tax planning: what it is and how to do it in your company

- CLM Controller English Blog

Conclusion

Brazil transfer pricing is now a strategic issue for multinationals, not a mechanical calculation. The country has moved toward an OECD-aligned arm’s length model, which means Brazilian entities must be able to explain their role in the group value chain and support the prices used in cross-border related-party transactions.

For multinational groups, the safest approach is to review contracts, pricing policies, documentation, accounting segmentation and tax reporting before the Brazilian operation grows. The new rules create more alignment with global standards, but they also demand stronger evidence and better coordination between local and global teams.

| Need support with transfer pricing in Brazil? CLM Controller helps multinationals operating in Brazil with tax consultancy, transfer pricing reviews, documentation support, accounting alignment, international tax risk mapping and compliance routines. If your group has cross-border related-party transactions involving Brazil, talk to CLM Controller before tax adjustments become tax exposure. |

FAQ: Brazil transfer pricing rules for multinationals

When did Brazil’s new transfer pricing rules become mandatory?

The new OECD-aligned rules became mandatory from 2024. Taxpayers had an option to adopt them early for 2023 if they followed the required procedure.

Which taxes are affected by Brazilian transfer pricing?

The rules affect the calculation of IRPJ and CSLL for Brazilian entities engaged in controlled transactions.

Do the rules apply only to goods?

No. They cover goods, services, intangibles, commodities, financial transactions, cost contribution arrangements, business restructurings and other controlled transactions.

What is the arm’s length principle?

It is the principle that related-party cross-border transactions should be priced and structured as independent parties would agree under comparable circumstances.

Is a Master File required in Brazil?

Depending on the total value of controlled transactions, Brazilian taxpayers may need to submit Master File and Local File documentation. Thresholds under the RFB framework distinguish exemptions, simplified files and complete files.

Can a multinational use its global transfer pricing policy in Brazil?

Yes as a starting point, but it must be checked against Brazilian law, local facts, accounting data, tax returns and documentation requirements.

Are low value-added services automatically safe with a 5% markup?

No. The simplified approach only applies when the service meets the low value-added criteria. Core services, R&D, manufacturing, marketing, sales, financial transactions and high-value intangible services generally require deeper analysis.

Sources consulted

- Receita Federal – New rules for taxation of multinationals with presence in Brazil

- Receita Federal – Public consultation on transfer pricing regulations

- Receita Federal – Commodity controlled transactions consultation

- Receita Federal – RTC guidance for commodity transactions

- OECD – Transfer pricing

- CLM Controller – Accounting tax consultancy

0 Comments